General Guidelines

Your firm is in the market to raise capital. You selected an investment banker to represent you in the process. The firm’s vision, financial goals, strategy and performance have been documented for the investors to review. An information library, stocked with materials such as a flip book, financial statements, standard forms and contracts, company policies and procedures, and a financial model is available to potential capital providers upon signing an NDA. The preparation of these materials took weeks or perhaps months. Your banker sorted through his/her contact list of investors making dozens even hundreds of preliminary investor calls. This resulted in a short-list of potentials that want to setup a conference call with your company’s top management.

Initial investor call

At this point, the many weeks and months of work are finally paying off. Surely, the investor will recognize the opportunity of marketplace lending/fintech and want to invest, right? Maybe, but remember the process is only getting started. Often company managers become hasty thinking all the preliminary work means a deal is close to consummation. For this reason, I always remind the client that the initial investor call is not to discuss the terms a deal. One should introduce themselves and the company, provide substance to certain key metrics and outline the firm’s overall strategy. Yet, I continually witness clients outline terms or discuss valuation too early in the conversation. This may make an investor feel pressured, suggest price shopping or even worse make your company appear desperate during the call. For an investor’s point-of-view, this suddenly appears like a low-probability transaction. That pushes them away from your opportunity in favor of others.

Deals gain momentum throughout the process. Therefore, it’s important that companies executives continue building rapport with potential capital providers. Setting terms or deadlines too early may derail the momentum and work to your disadvantage. It’s a fragile balance keeping investors on track without pushing them too hard. This is a paradox for companies who try to capitalize from the immense investor interest for marketplace loans and fintech solutions by forcing answers before investors are ready.

Have a capital plan that matches your investor

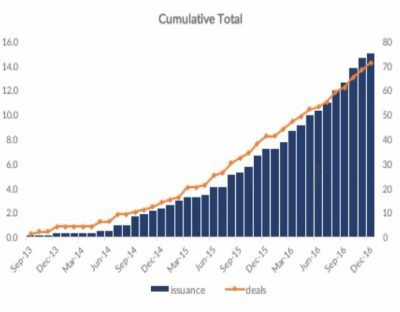

What happened after the first-ever securitization of marketplace loans in the United States for Eaglewood Capital Management is phenomenal! From these deals, ECLT 2013–1 and ECLT 2014–1, came a flood of issuers Avant, Earnest, Marlette, Lending Club, Loan Depot, and Social Finance to name a few. PeerIQ estimates a cumulative issuance over $15bn at year-end 2016 (see graph) and an additional $6.3 — $11.2bn expected for 2017. The market is not only growing at an astounding pace, 50% or more annualized growth, but by all measures here to stay.

New set of investors

Angel investors, venture capital and private equity were the predominant form of capital just a few years ago. Now, securitization brings a new set of investors to the space. Money managers, insurance companies, banks, endowments, pensions, investment banks and others can now participate through the securitization market. That is a tremendous opportunity for marketplace lenders and fintech companies alike as access to these investors offers unlimited scalability and diversified sources of funding. It also demonstrates a general acceptance by the industry that there is a shift in the way financial services are delivered. Undoubtedly, this impacts technology providers as well as marketplace lenders.

Along with this new investor base come a different set of questions. For example, the focus for an early stage equity investor typically centers on strategy, scalability and making a multiple on their investment. Expect questions that reflect these concerns.

Be prepared to discuss:

- growth constraints

- origination volumes

- market size

- technology

- partnerships

Or other items relevant to the party’s investment objective.

Work with your investment banker to develop potential exit strategies for the investor. Have them evaluate the potential upside of your business along with the corresponding metrics for valuation. Develop a narrative on the market opportunity and how your company is positioned to monetize from it. Early stage capital is available for companies with huge promise. Until few years ago, it was the primary source of capital to marketplace lenders.

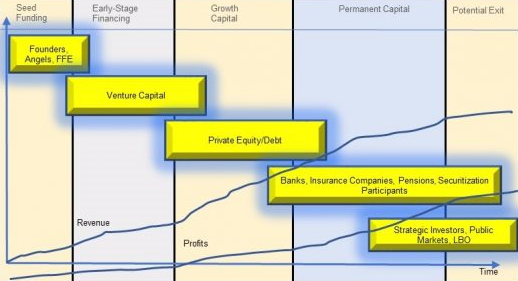

Diagram: Distinguishing Forms of Capital

Public markets

Access to the public markets is a game changer. Securitization issuers and public companies benefit from cheaper sources of funding and the ability recycle their capital in exchange for standardizing procedures and disclosures. Correspondingly, we now have years of performance data based on billions of dollars of marketplace loans. Public listings are another source of information as the whole world can tap into the financial performance of a publicly listed company. This changes the conversation completely. If your company is this far along, expect questions such as:

- underwriting guidelines

- collection procedures

- estimated loan losses

- reporting procedures

- cost of funding

- profitability

- performance measures

- capital markets plans.

Do homework on others and play into your strengths as an organization whether it’s underwriting, marketing, funding, growth potential, operational performance, customer acquisition cost, profitability, personnel or technology. Information is becoming more and more available and so as the industry evolves so should you. Be prepared and use your investment banker as a resource.

Allow the Investor to make their pitch

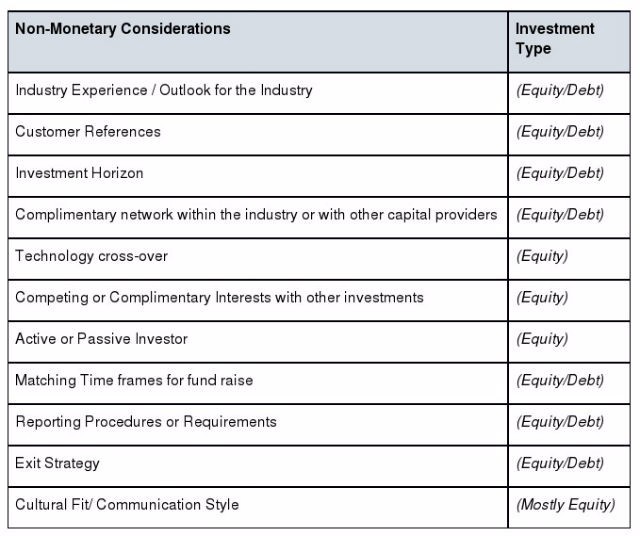

Let the investor talk. Beyond just being polite, listening enables one to learn more about a potential capital partner. This is not to be underestimated, especially with equity investors, who may have different visions for the company. Board meetings may already be challenging, and you want differences discussed before adding a new shareholder. If it is debt you seek, remember banks and debt holders can also be fickle. Too many times, we received investor calls from clients after banks, loan-flow partners or other creditors abruptly decide to leave a line-of-business or call a loan. So, while money is fungible, it may not be the only asset that a capital provider brings. Remember to be a good listener and ask questions that help evaluate non-monetary considerations such as cultural fit or strategic match. Your investment banker can often help by sharing their personal experiences with an investor.

Save the Structuring for Later

Don’t be discouraged by those who aren’t prepared to discuss details on the first call. The purpose of the initial discussions is to get to know the investor(s) and discuss high-level issues and concerns. Chances are that the counterparty has some interest but has not yet budgeted the time to dive into the materials. Why else would they be on the investor call?

Do not cause deal fatigue. Answer due diligence questions honestly but defer valuation questions to your banker. The banker should guide you regarding the timing of discussions related to deal terms. Don’t take anything for granted until you receive an offer in writing; continue talking to other parties until you execute a formal indication of interest. The investment banker will help you compare and analyze offers once received.

This is merely a guideline to help maximize your probability of success. Of course, every situation is unique. Try not to get frustrated with the process. It may seem time-consuming and difficult but good deals don’t come easy. I hope you find the above helpful in finding a suitable investment partner and maximizing shareholder value.

Author:

Written by Phil Toth, Managing Director of Oberon Securities